Just how to Choose the Right Mortgage Loan Officer California for Refinancing Your Home

Recognizing the Fundamentals of Safeguarding a Mortgage for Your New Home

Starting the trip to protect a home mortgage finance for your new home needs an extensive grip of several basic elements. The range of home loan kinds, nuances of interest rates, and the essential duty of credit rating all contribute to the intricacy of this procedure. As you browse the myriad of options and requirements, understanding how these components interaction can be essential to your success. Yet, what genuinely equips possible home owners is usually neglected. Could there be a crucial strategy that simplifies this seemingly daunting venture? Allow's explore how to effectively approach this vital economic decision.

Sorts Of Mortgage

Browsing the varied landscape of home loan is important for potential homeowners to make educated economic decisions - mortgage loan officer california. Understanding the different kinds of mortgage readily available can dramatically influence one's choice, straightening with economic objectives and personal scenarios. One of the most usual types consist of fixed-rate, adjustable-rate, FHA, VA, and jumbo finances, each serving distinctive needs

For individuals with restricted deposit capabilities, Federal Housing Management (FHA) fundings provide a viable alternative, calling for reduced down payments and credit score ratings. Professionals and active-duty armed forces members may get VA fundings, which supply competitive terms and commonly require no deposit. Jumbo fundings cater to purchasers in high-cost locations seeking to fund properties going beyond standard funding restrictions.

Picking the right mortgage type includes assessing one's economic stability, future strategies, and comfort with threat, ensuring a well-suited pathway to homeownership.

Recognizing Rates Of Interest

A fixed passion rate continues to be continuous throughout the loan term, using predictability and security in month-to-month settlements. In contrast, a variable or adjustable-rate home mortgage (ARM) might begin with a reduced passion price, but it can change over time based on market problems, possibly increasing your payments dramatically.

Rates of interest are mostly affected by economic aspects, including rising cost of living, the Federal Get's monetary plan, and market competition among lending institutions. Debtors' credit report and monetary accounts likewise play an essential role; greater credit rating commonly secure reduced rates of interest, mirroring reduced risk to lenders. Improving your credit rating score prior to applying for a home mortgage can result in considerable savings.

It's vital to compare deals from multiple lending institutions to ensure you safeguard the most positive price. Each percentage point can influence the lasting cost of your mortgage, underscoring the relevance of extensive research study and notified More Info decision-making.

Lending Terms Explained

A key aspect in comprehending mortgage contracts is the loan term, which dictates the period over which the borrower will pay off the funding. Commonly expressed in years, lending terms can substantially influence both regular monthly repayments and the total rate of interest paid over the life of the funding. One of the most typical home loan terms are 15-year and 30-year durations, each with unique advantages and considerations.

A 30-year lending term enables for reduced monthly payments, making it an attractive choice for numerous homebuyers seeking affordability. Nonetheless, this prolonged payment duration commonly causes greater total interest prices. On the other hand, a 15-year car loan term typically includes greater regular monthly repayments but uses the advantage of reduced rate of interest accrual, making it possible for home owners to build equity quicker.

It is essential for debtors to evaluate their financial circumstance, long-term objectives, and threat tolerance when selecting a car loan term. Furthermore, comprehending various other aspects such as early repayment penalties and the potential for refinancing can provide further adaptability within the picked term. By meticulously taking into consideration these components, borrowers can make enlightened choices that line up with their economic purposes and make certain a workable and effective home mortgage experience.

Relevance of Credit History

Having a good credit report can substantially affect the terms of a home loan. Debtors with greater ratings are normally offered lower rate of interest, which can cause substantial cost savings over the life of the funding. Furthermore, a strong credit report might enhance the chance of finance authorization and can give greater negotiating power when discussing funding terms with lenders.

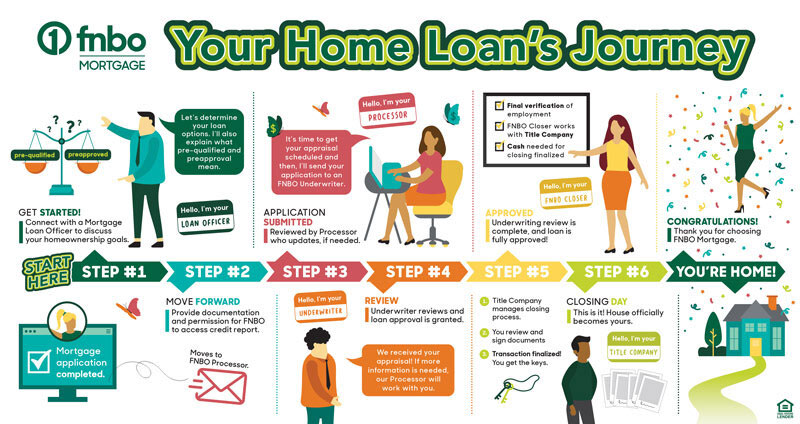

Navigating the Application Refine

While credit rating play a critical role in safeguarding a home loan, the application process itself calls for careful navigating to make certain an effective result. The procedure starts with gathering essential documentation, such as proof of revenue, tax returns, bank statements, and recognition. This documentation provides i loved this loan providers with a comprehensive view of your monetary security and capability to repay the finance.

Following, research different lenders to compare rate of interest, lending terms, and charges. This action is vital, as it aids determine one of the most desirable home loan terms tailored to your monetary scenario. As soon as you have actually selected a lender, finishing a pre-approval application is a good idea. Pre-approval not only strengthens your negotiating power with vendors but also offers a precise photo of your borrowing ability.

Throughout the home mortgage application, make certain accuracy and completeness in every information provided. Mistakes can result in delays and even rejection of the application. Furthermore, be planned for the lending institution to ask for more details or explanation throughout the underwriting procedure.

Conclusion

Protecting a mortgage finance requires a detailed understanding of numerous elements, consisting of the types of loans, rate of interest rates, financing terms, and the role of debt ratings. Effective navigation of these aspects is essential for a successful home loan application process.